Author Archives: Moneythor Team

What Could Go Wrong? The Benefits and Pitfalls of Behavioural Science in Banking

Moneythor Behavioural Science Series with Klaus Wertenbroch. Moneythor’s behavioural science series, a four-part collection of [...]

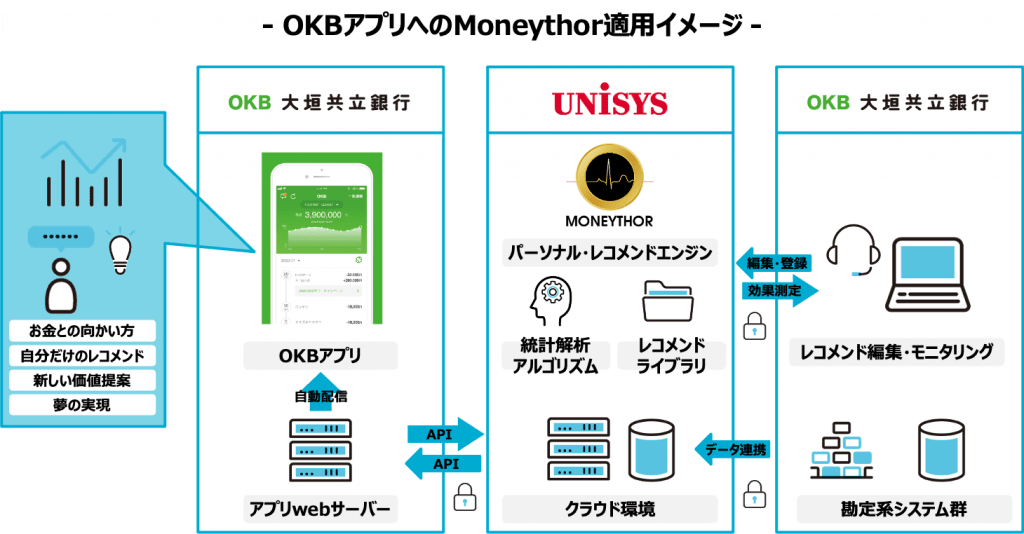

Moneythorが大垣共立銀行に採用されました

Moneythor製品が大垣共立銀行にご採用いただいくことが決まりましたのでご報告させて頂きます。大垣共立銀行、日本ユニシス、Moneythorの3社は、国内初の事例となる2021年度の導入を目指し、パーソナルレコメンドサービスの提供に向けた共同プロジェクトを始動しました。 オンライン・非接触などのアフターコロナ後のニューノーマルが浸透し金融サービスのDX(デジタルトランスフォーメーション)が求められる中、従来から “スマートなお金の管理” をサポートする公式アプリ「OKBアプリ」を展開し、個人のお客さまに向けたデジタルサービスを提供している大垣共立銀行は、この度「OKBアプリ」のより一層の高度化を図り、お客さま一人ひとりのライフスタイルに寄り添った提案(パーソナルレコメンド)を通じた双方向型の新しい関係性を構築することを目指し、「Moneythor」の採用を決定しました。 「Moneythor」は統計的アルゴリズムや機械学習を用いて、金融機関が有する膨大な取引データからお客さまの消費パターンや資産状況を自動で分析し、使い過ぎに対するアラートや節約のアドバイス、余剰資産を活用した投資の促進など、グローバルで実績のある豊富なライブラリを活用しながら最適なコンテンツをあらゆるデジタルチャネルに自動配信できるサービスです。 本プロジェクトにおいて、マネーソーは日本ユニシスと共同でMoneythor製品をご提供致します。「OKBアプリ」にMoneythorを連携することで、大垣共立銀行は保有するお客さまの膨大な取引データなどを活用して、家計の使いすぎアラートや余剰資金を活用した積立投資シミュレーションなど、お客さま一人ひとりに寄り添った「お金との向き合い方」をご案内します。個人の嗜好やライフスタイルを分析し、最適な家計管理や資産形成をご提案しながらOKBとお客さまとの中長期的な繋がりを構築することを目指します。 大垣共立銀行の安田次朗執行役員IT統轄部長のコメント 「人生100年時代のお金に関する不安を解消し、より豊かな生活づくりをサポートするためMoneythorの導入を決定しました。マネーソーのデータアナリティクスエンジンを活用することで、お客様にパーソナライズされた気づきや助言を提供し、リアルとデジタルが融合する社会で、お客様が真に求めるサービスを追求していきます。」 日本ユニシス株式会社の竹内裕司執行役員ネオバンク戦略本部長のコメント 「この度の大垣共立銀行様に向けたMoneythor提供を、心より喜ばしく感じております。弊社は、従来培ってきたICTノウハウを活用し、金融機関のデジタル・トランスフォーメーションを支援すると同時に、生活者一人ひとりに寄り添った新しい金融サービスの提供を進めております。マネーソー様とのパートナーシップの元、この取り組みを更に深化することで大垣共立銀行様が目指すデジタル・イノベーションに貢献して参ります。」 マネーソー共同創業者兼CEOオリビエ・ベルティエのコメント 「大垣共立銀行様は顧客の視点に立ち顧客のニーズに応えるデジタル体験を提供することにコミットした先見的な銀行だと認識しています。その大垣共立銀行様に、パーソナライズしたデータドリブンな顧客体験を提供するため弊社を日本ユニシス様とのパートナーシップを通じてご採択いただいたことを大変嬉しく思います。」 【今後の取り組み】 弊社は、Moneythorの提供を通じて大垣共立銀行のデジタル・トランスフォーメーションを日本ユニシスとともにご支援致します。 また今後はこのような取り組みを全国の金融機関に向けて幅広く展開することで、顧客関係の強化を図りたい金融機関が今後お客様のニーズに応えられるようデジタルチャネルを改善する際の強力なサポーターとなり、お客様にとって家計・資産管理をもっと身近にするお手伝いをしていきます。 ■大垣共立銀行について [...]

Ogaki Kyoritsu Bank Selects Moneythor to Enhance its Digital Banking Services

Moneythor, an award-winning provider of data-driven digital banking software, in partnership with Nihon Unisys, has [...]

What are APIs? | Digital Banking 101

The term Application Programming Interfaces (APIs) first emerged at the beginning of the 2000’s in [...]

A Guide to Personalisation in Banking

Table of Contents 1. What is Personalisation in Banking? 2. Benefits of Personalisation in Banking [...]

When Banking and Behavioural Science Collide

Moneythor Behavioural Science Series with Klaus Wertenbroch. Moneythor’s behavioural science series, a four-part collection of [...]

Standard Chartered Partners Moneythor to Deliver its Personal Financial Management Tool

Standard Chartered Bank in Singapore has partnered Moneythor, a leading digital banking software provider, to [...]

Banking-as-a-Service (BaaS)

What is Banking-as-a-Service? Banking-as-a-service (BaaS) is an end-to-end process where third parties – finTech, non-finTech, [...]

What is Sustainable Finance?

Environmental issues and climate change have never been so topical and there is a growing [...]

Information Avoidance | Behavioural Science in Banking

How often do you read the terms and conditions when downloading a new mobile app [...]

Benefits of Offering an Adult/Child or Junior Account

Financial literacy and money management are not always part of the school curriculum and most [...]

Hyperbolic Discounting | Behavioural Science in Banking

We have all been there, our plans to eat healthily or save for the future [...]

Global Open Banking 2.0

In 2019 we launched our first global Open Banking report to take a look at [...]

データで見る:新型コロナがオンラインバンキング利用を促進し顧客心理を変えた

企業イノベーションを実現するのは誰でしょう。社長ですか?イノベーション戦略室長ですか?答えは「新型コロナ」。冗談交じりにこう語られる場面に出会ったことはないでしょうか。その冗談が今、現実になりつつあると言えます。少なくとも消費者の心理・行動には明らかな変化が見えてきています。 図表1. Source: McKinsey & Company 2020年6月29日“Financial Decision Maker Sentiment”のデータをもとに日本語訳とJapanの結果追加。 新型コロナの感染拡大を受け外出の自粛が始まった今年3月、三菱UFJ銀行のインターネットバンキングの新規利用者が前年同月比の3倍、またアプリ経由の口座開設がみずほ銀行では前年同月比の6割増、りそなグループ銀行では2倍だったというように、新型コロナがオンラインバンキング利用を後押ししたことが明らかになっています。 しかしこれは一時的なことなのでしょうか。コロナ収束後の人々の行動がどうなるのかが気になるところですが、今年4月から6月に行われたMcKinsey & Companyのアンケートによると世界各国共通して、コロナ収束後、オンラインやモバイルバンキングを「コロナ前よりもっと利用するだろう」と答えた人が多く、また支店は「コロナ前より利用しないだろう」と答えた人が多くいるという興味深い結果になっています。(図表1) 同上のアンケート調査の中で、自分が利用する銀行やカード会社に何を期待しているのかを問う質問に対しては、日本の回答者の40%以上が「全ての手続きがオンライン上でシームレスに行えるようオンラインチャネルを改善して欲しい」と回答しています。(図表2) [...]

Digital Banking 101

Digital Banking involves the digitalisation of traditional banking services such as current accounts, credit cards, [...]

The Fresh Start Effect | Behavioural Science In Banking

Have you ever wondered why New Year’s resolutions are so popular? It turns out that [...]

Post-pandemic Digital Banking for SMEs

The statistics about the expected survival rates of SMEs post the COVID-19 pandemic are worrying. [...]

Anchoring Bias | Behavioural Science In Banking

When it comes to making a purchase or financial decision people often use an anchor, [...]

How Carbon Footprint Insights can Enhance Digital Banking

The world looks a lot different in May 2020 than it did in May 2019. [...]

Goal Priming | Behavioural Science In Banking

There is a constant internal battle between our best intentions and our sudden impulses. As [...]