Cashless payments are internationally the preferred method of transaction today. This has not only been supported by developments in financial technology and digital banking, but Covid-19 has moved people towards “minimal contact” options for transactions and payment. This move to cashless systems has also had an impact on consumers buying and spending behaviours.

What is the Cashless Effect?

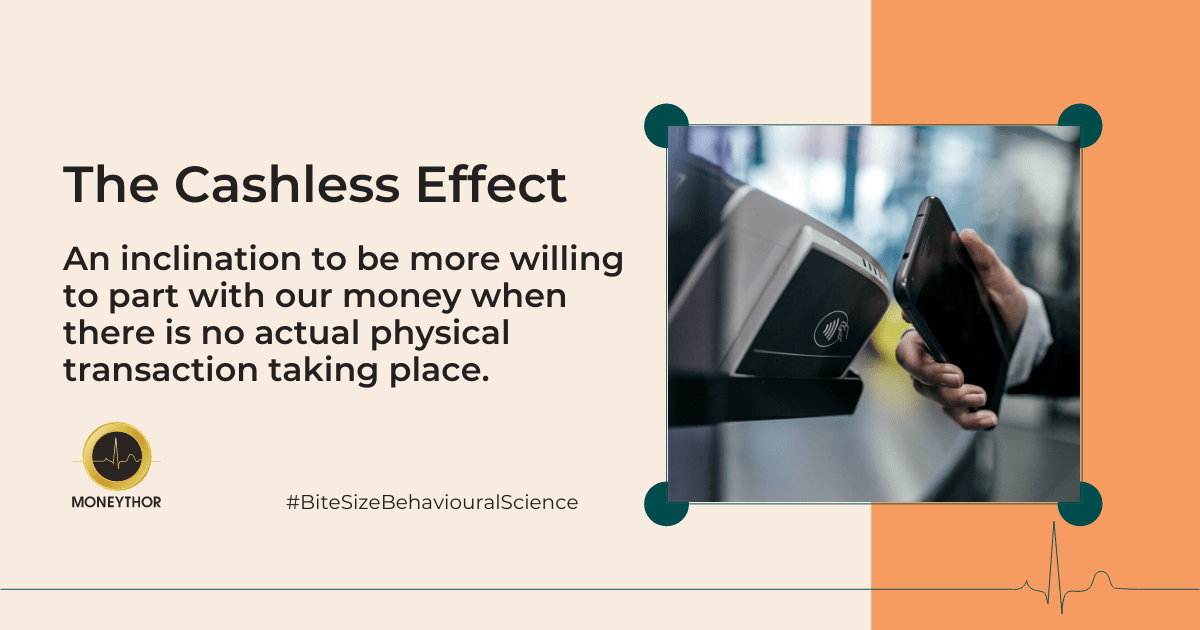

The Cashless Effect is a cognitive bias that characterises an inclination to be more willing to part with our money when there is no actual physical transaction taking place. Essentially, we are more likely to spend more money when we are not spending physical cash, as it more abstract and therefore less psychologically painful to part with.

The “pain of paying” is a typical negative emotion to go through when paying with physical currency. However, tapping or swiping a card and the absence of tangible cash takes the edge off quite easily. Digital payments create a form of disassociation from the negative arousal we tend to feel from parting with cash, and as it becomes a primary way which we make transactions, it becomes easier to overspend and make higher risk purchases that we typically would.

What can financial institutions do to help consumers be aware of the Cashless Effect?

Monthly notifications for auto-debit payments and subscriptions

In addition to cashless transactions at the point of sale or e-commerce store, it is also common for consumers to set up auto-debit for recurring payments and subscriptions today. Auto-debiting as a default is a shortcut that enables consumers to very easily forget that they are in fact paying for services or subscriptions that they perhaps no longer require. Regular notifications for new, upcoming or soon-to-renew auto-debit payments can be a useful way to help users track their spending, understand what they are paying for and gives them the opportunity to cancel if they no longer require the subscription.

Money management tools

As cashless payments become the norm, it is important that banks provide users with timely spend tracking features allowing them to understand their finances better and help with ensuring that they don’t overspend. From setting up budgets, financial forecasting capabilities that analyses spending habits, visuals that provide users with an understanding of their regular payments’ schedules, to automated settings that divest a predetermined amount for savings regularly, banks can provide users with actionable and personalised money management tools to continually review their finances, hence providing some control over the Cashless Effect, despite the instrument’s many undeniable benefits in terms of convenience.

Increasing friction for big expenses

Cashless payments remove effort and friction from the purchasing process, thus further eliminating the pain of paying. Payment methods like Apple Pay, Google Pay and Amazon 1-click have revolutionised the payment process, doing away with even the use of cards while checking out.

By increasing friction for users who want to pay with cashless methods especially for online purchases and big expenses, consumers can be compelled to take a moment to consider the amount they are paying for the items they want to buy, thus giving them the chance to reconsider their purchases.

Furthermore, if a buyer is overstretching their budget, this moment of pause gives them the opportunity to confirm that they indeed want to go through with the payment despite the negative arousal they might feel.

In addition to their inherent security benefits, friction points in digital banking are created through means such as the requirement of one-time passwords (OTP) sent to users via text or needing to launch digital banking apps to verify payments. It can also be a requirement to pay with an alternate method for larger payments. While these methods might seem cumbersome to users on a day-to-day basis (again, notwithstanding their security benefits), it brings back a form of acknowledgement to payments, thus inciting a more tangible feeling of parting with money which hopefully enables more informed decision making.

Conclusion

Cashless payments are a wonderful convenience for consumers and are here to stay. Having said that, financial institutions should help consumers stay on top of their finances and be informed about their financial situation regularly to curb the overspending side effect which this seamless payment method may generate. The Cashless Effect should be considered by financial institutions when building out financial wellbeing programs and personal financial management (PFM) tools as well, to ensure a more cohesive approach being taken by all stakeholders involved in order to offset the consequences it may pose to users in the long run.