What is the Goal Gradient Effect?

Whether we are acting as students, employees or consumers, our efforts towards completing a goal accelerate drastically the closer we are to achieving it. As human beings, there is a tendency for us to be more motivated by how much remains to complete a goal, rather than how far we have come. There is a correlation to the commitment we have invested in an opportunity, which is why consistency and commitment are strong motivators in the completion of any task.

The goal gradient effect was originally proposed by pioneer behavioural psychologist Clark Hull in 1934. He conducted an experiment on rats to test his theory, and found that they ran progressively faster as they approached the food at the end point. This theory indicates a classic finding from behaviourism: animals put in more effort as they near a reward. Building on this theory, behavioural scientists began to generate new propositions about human psychology in relation to rewards, and the implications on consumer behaviour in general.

Studies have also shown that the goal gradient effect has a direct impact on our social psyche and motivation. For example, people are more likely to contribute as charitable campaigns approach their goals. Late stage efforts allow donors to feel a greater degree of perceived impact, a heightened level of satisfaction with their generosity and fulfilment from having personal influence in solving a social problem.

How can financial institutions use the Goal Gradient Effect to help consumers develop better financial habits?

Remove barriers to entry and incentivise customers

Marketing specialist Guy Kawasaki once quipped that “the hardest part about getting started, is getting started”. For a range of reasons, consumers find themselves hesitating when it comes to developing better habits, financial or otherwise. Targeted use of incentives is a great way to get customers “out of the starting blocks” and on the way to achieving their goals. Once consumers are on the path towards their goal, the likelihood of them achieving success increases considerably. The goal gradient can be used in this situation, whether through loyalty programmes or in making investment funds attractive to customers, to incentivise the initial uptake.

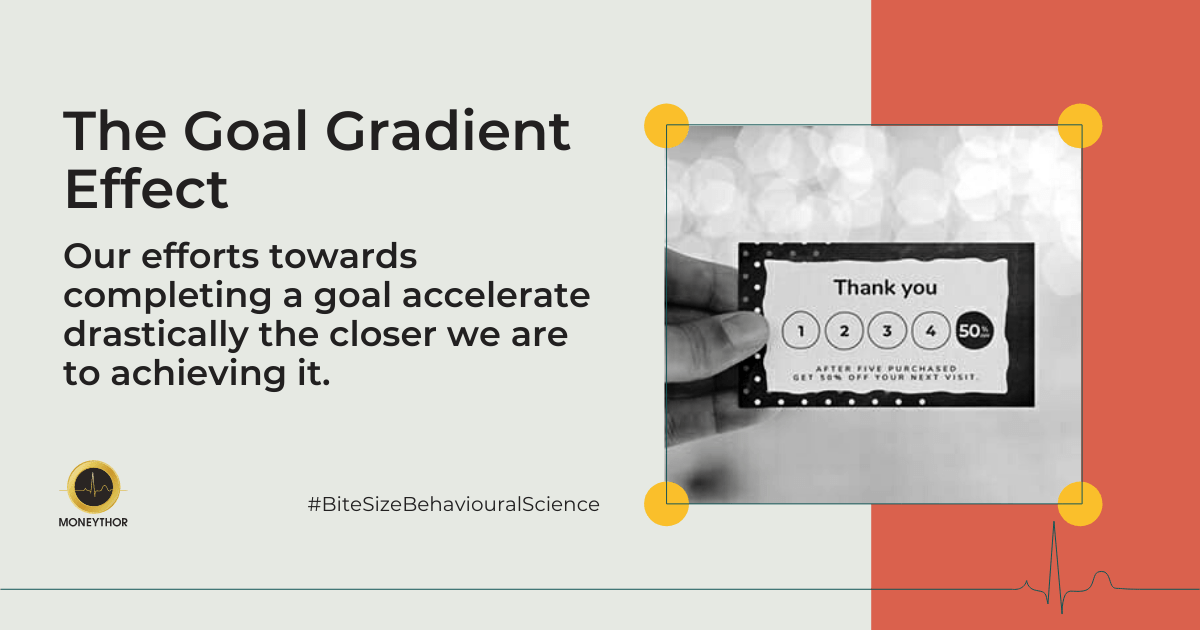

Visuals as a motivating factor

Envisioning progress towards a goal induces an increment in the speed of completion. PFM solutions including saving goals allow customers to watch the rate at which they are saving, thus heightening their desire to finish. Additionally, reminders and nudges when a customer has reached a milestone have the potential to motivate them further.

While the ratio of benefit to the remaining cost increases as we approach a goal, levels of effort are also expected to decline once a goal has been achieved. How do we then ensure sustainability and longevity in the newly formed financial habit of saving? In this case, a suggestion or ideas for the next big thing to save for might help consumers keep up with their newly formed good habits, and ideally also help them achieve financial wellbeing in the long run.

Reframing goals and making them achievable

The motivation to achieve a goal is directly related to its size. For example, a customer wants to save $400 a month. Instead of telling them to set aside $100 a week, an option is to break it down to $14.30 a day. Not only does the figure appear more achievable, the customer will also be able to compare that amount to the price of a movie ticket, a fast food meal and the choice of a taxi versus public transport. Suddenly, the idea of saving $400 a month seems all the less daunting. Moving the goalpost forward not only increases motivation, it also helps with a daily sense of accomplishment and gives the customer an instant physiological reward.

Conclusion

Consider the Goal Gradient Effect when implementing new loyalty programmes, building personal financial management solutions centered around savings and financial wellbeing programmes. Remove barriers to entry and incentivise users to begin with whilst ensuring they can see how far they’ve come. Breaking down goals helps them appear achievable and gives consumers a regular sense of accomplishment to help them stay motivated. It is easy to focus on what is left to achieve but getting there is made easier when you can appreciate how far you have already come.